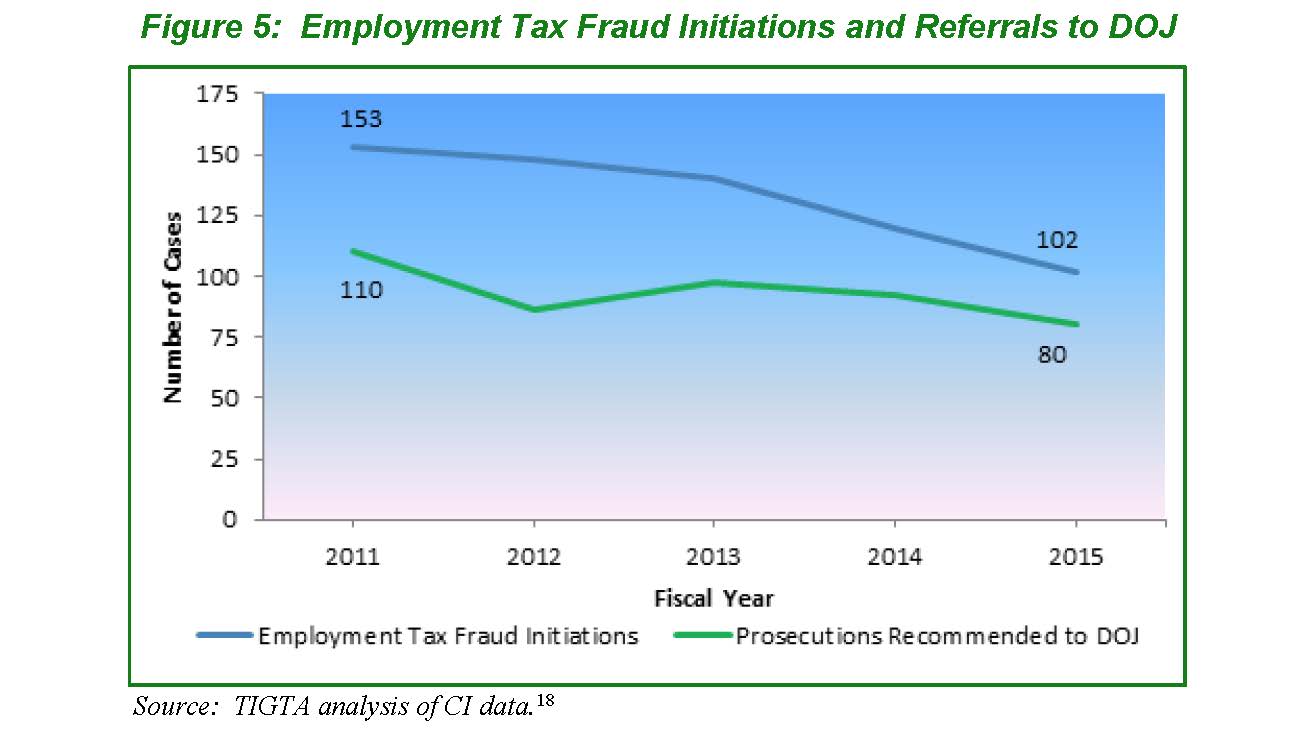

CI Employment Tax Investigations 2011-2015

Employment tax investigations represent a small portion CI casework. For example, in FY 2015, CI initiated 102 employment tax investigations, which is less than 3 percent of all initiated cases. In comparison, the top two priorities—identity theft and abusive return preparer fraud and questionable refund fraud—resulted in almost 1,800 new investigations and accounted for 47 percent of new initiations in FY 2015. Figure 5 shows the number of employment tax cases initiated and referred for prosecution from FYs 2011 through 2015.

n18 Since actions on a specific investigation may cross fiscal years, the data shown in cases initiated may not always represent the same universe of cases shown in other actions within the same fiscal year.

Sources of CI Employment Tax Investigations 2011-2015

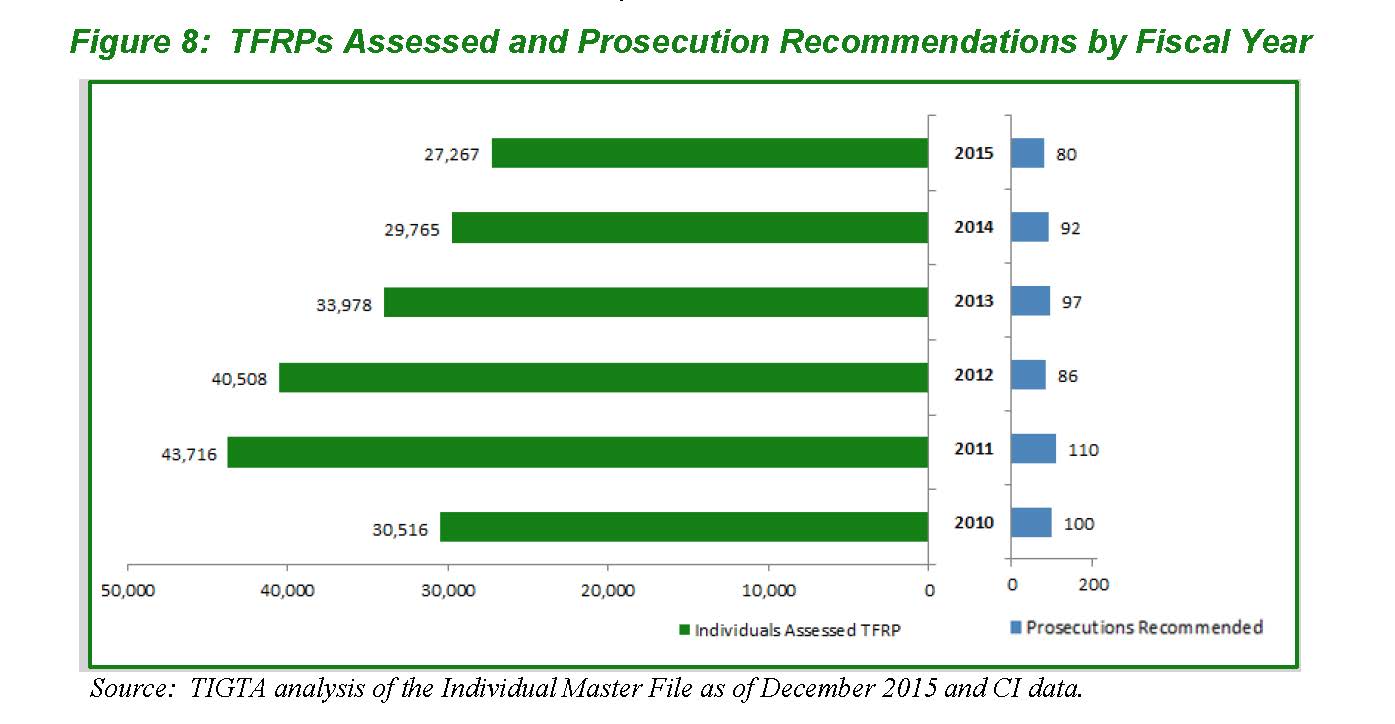

TFRP and CI Employment Tax Investigations 2010-2015

IRS Civil Division Fraud Referral Process

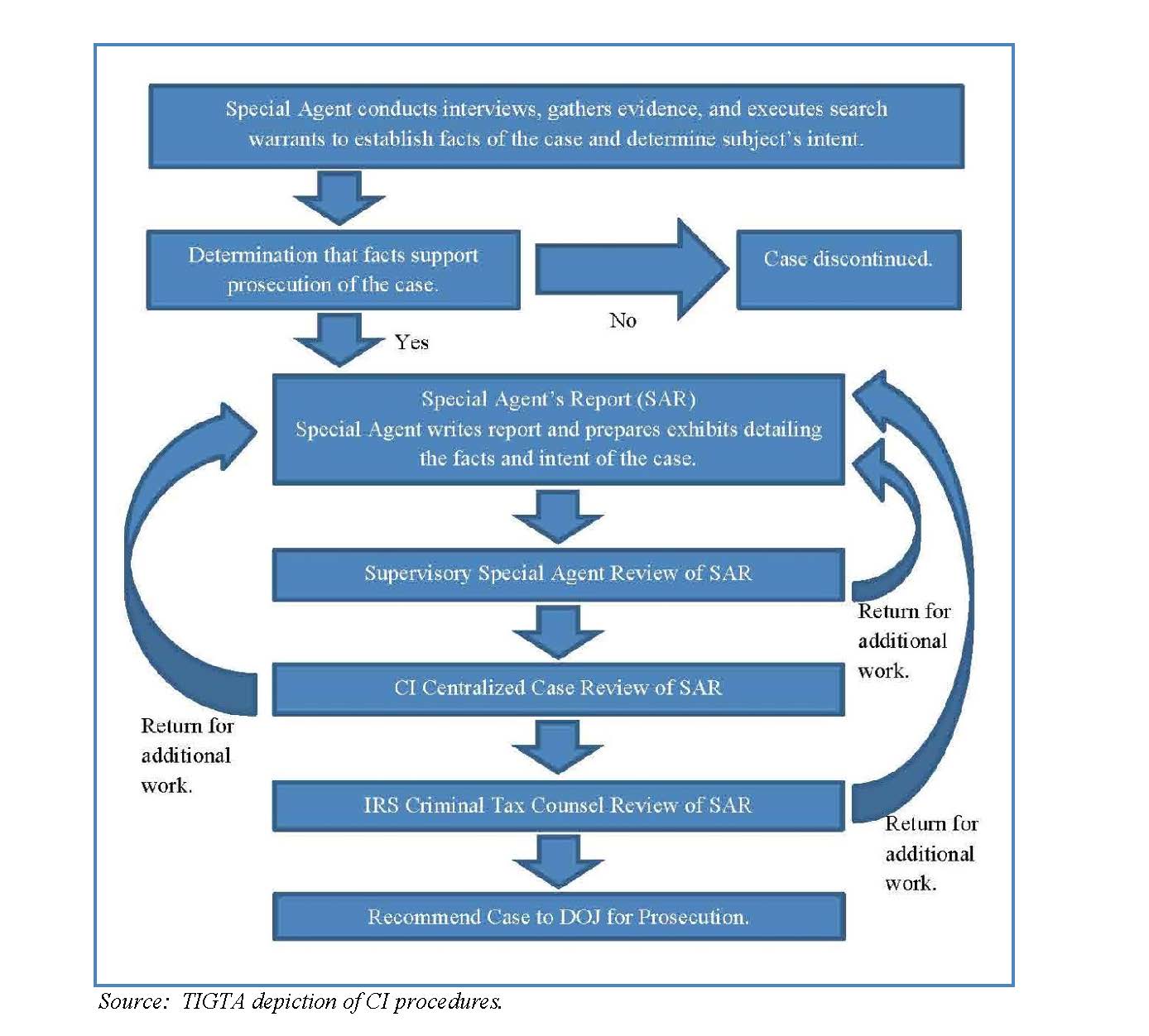

IRS CI Investigation and DOJ Referral Process

No comments:

Post a Comment

Please make sure that your comment is relevant to the blog entry. For those regular commenters on the blog who otherwise do not want to identify by name, readers would find it helpful if you would choose a unique anonymous indentifier other than just Anonymous. This will help readers identify other comments from a trusted source, so to speak.